CHINT – CHINT ELECTRIC 2023 ESG Report Highlights Analysis

CHINT ELECTRIC 2023 ESG Report Highlights Analysis

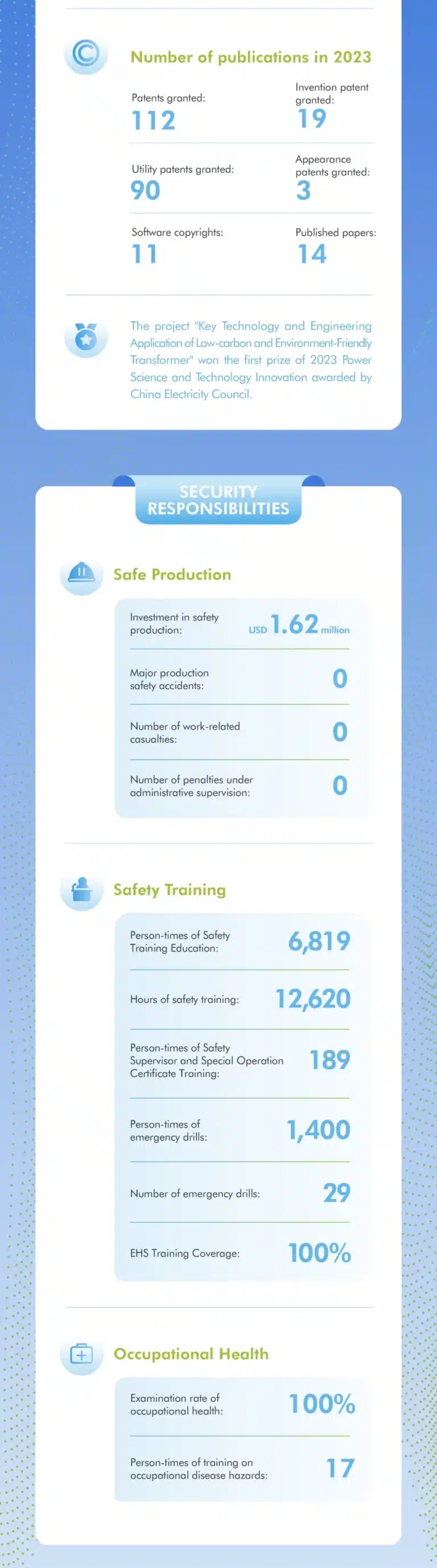

SourceCHINT Global

EMR Analysis

More information on CHINT: See the full profile on EMR Executive Services

More information on Nan Cunhui (Chairman, Zhengtai Group + Chairman, CHINT Group): See the full profile on EMR Executive Services

More information on Lily Zhang (Executive President, CHINT Electric + President and Chief Executive Officer, CHINT Global): See the full profile on EMR Executive Services

More information on Sustainability by CHINT: See the full profile on EMR Executive Services

More information on the 2023 ESG and CSR Report by CHINT: See the full profile on EMR Executive Services

More information on Net Zero by 2050 by the United Nations: https://www.un.org/en/climatechange/net-zero-coalition + Put simply, net zero means cutting greenhouse gas emissions to as close to zero as possible, with any remaining emissions re-absorbed from the atmosphere, by oceans and forests for instance.

Currently, the Earth is already about 1.1°C warmer than it was in the late 1800s, and emissions continue to rise. To keep global warming to no more than 1.5°C – as called for in the Paris Agreement – emissions need to be reduced by 45% by 2030 and reach net zero by 2050.

More than 140 countries, including the biggest polluters – China, the United States, India and the European Union – have set a net-zero target, covering about 88% of global emissions. More than 9,000 companies, over 1000 cities, more than 1000 educational institutions, and over 600 financial institutions have joined the Race to Zero, pledging to take rigorous, immediate action to halve global emissions by 2030.

More information on Net Zero by 2050 by the Science Based Targets initiative (SBTi): https://sciencebasedtargets.org/net-zero + The SBTi’s Corporate Net-Zero Standard is the world’s only framework for corporate net-zero target setting in line with climate science. It includes the guidance, criteria, and recommendations companies need to set science-based net-zero targets consistent with limiting global temperature rise to 1.5°C.

UN vs. SBTi:

- UN targets nations, while SBTi focuses on companies. UN sets a broad goal, while SBTI provides a detailed framework for target setting.

- Both aim to achieve net zero emissions and limit warming to 1.5°C. The UN sets the overall direction, and SBTi helps businesses translate that goal into actionable plans.

Key components of the Corporate Net-Zero Standard:

- Near-term targets: Rapid, deep cuts to direct and indirect value-chain emissions must be the overarching priority for companies. Companies must set near-term science-based targets to roughly halve emission before 2030. This is the most effective, scientifically-sound way of limiting global temperature rise to 1.5°C.

- Long-term targets: Companies must set long-term science-based targets. Companies must cut all possible – usually more than 90% – of emissions before 2050.

- Neutralize residual emissions: After a company has achieved its long-term target and cut emissions by more than 90%, it must use permanent carbon removal and storage to counterbalance the final 10% or more of residual emissions that cannot be eliminated. A company is only considered to have reached net-zero when it has achieved its long-term science-based target and neutralized any residual emissions.

- Beyond Value Chain Mitigation (BVCM): Businesses should invest now in actions to reduce and remove emissions outside of their value chains in addition to near- and long-term science-based targets.

EMR Additional Notes:

- ESG (Environmental, Social and Governance):

- Refers to the three key factors when measuring the sustainability and ethical impact of an investment in a business or company. Most socially responsible investors check companies out using ESG criteria to screen investments.

- ESG metrics are not commonly part of mandatory financial reporting, though companies are increasingly making disclosures in their annual report or in a standalone sustainability report.

- There is not a standardized approach to the calculation or presentation of different ESG metrics.

- Environmental: Conservation of the natural world

- Climate change and carbon emissions

- Air and water pollution

- Biodiversity

- Deforestation

- Energy efficiency

- Waste management

- Water scarcity

- …

- Social: Consideration of people & relationships

- Customer satisfaction

- Data protection and privacy

- Gender and diversity

- Employee engagement

- Community relations

- Human rights

- Labor standards

- …

- Governance: Standards for running a company

- Board composition

- Audit committee structure

- Bribery and corruption

- Executive compensation

- Lobbying

- Political contributions

- Whistleblower schemes

- …

- Environmental: Conservation of the natural world

- Criteria are of increasing interest to companies, their investors and other stakeholders. With growing concern about he ethical status of quoted companies, these standards are the central factors that measure the ethical impact and sustainability of investment in a company.

- Consequently, ESG analysis considers how companies serve society and how this impacts their current and future performance.

- CSR (Corporate Social Responsibility):

- Framework or business model that helps a company be socially accountable to itself, its stakeholders, and the public.

- The purpose of CSR is to give back to the community, take part in philanthropic causes, and provide positive social value. Businesses are increasingly turning to CSR to make a difference and build a positive brand around their company.

- CSR tends to target opinion formers – politicians, pressure groups, media. Sustainability targets here the whole value chain – from suppliers to operations to partners to end-consumers.

- CSR vs. ESG:

- CSR is a company’s framework of sustainability plans and responsible cultural influence, whereas ESG is the assessable outcome concerning a company’s overall sustainability performance.

- The major difference between them is that CSR is a business model used by individual companies, while ESG is a criteria that investors use to assess a company and determine if they are worth investing in.

- Carbon Dioxide (CO2):

- Primary greenhouse gas emitted through human activities. Carbon dioxide enters the atmosphere through burning fossil fuels (coal, natural gas, and oil), solid waste, trees and other biological materials, and also as a result of certain chemical reactions (e.g., manufacture of cement). Carbon dioxide is removed from the atmosphere (or “sequestered”) when it is absorbed by plants as part of the biological carbon cycle.

- Biogenic Carbon Dioxide (CO2):

- Biogenic Carbon Dioxide (CO2) and Carbon Dioxide (CO2) are the same. Scientists differentiate between biogenic carbon (that which is absorbed, stored and emitted by organic matter like soil, trees, plants and grasses) and non-biogenic carbon (that found in all other sources, most notably in fossil fuels like oil, coal and gas).

- Carbon Capture and Storage (CCS):

- CCS involves the capture of carbon dioxide (CO2) emissions from industrial processes. This carbon is then transported from where it was produced, via ship or in a pipeline, and stored deep underground in geological formations.

- CCS projects typically target 90 percent efficiency, meaning that 90 percent of the carbon dioxide from the power plant will be captured and stored.

- Decarbonization:

- Reduction of carbon dioxide emissions through the use of low carbon power sources, achieving a lower output of greenhouse gasses into the atmosphere.

- Carbon Footprint:

- There is no universally agreed definition of what a carbon footprint is.

- A carbon footprint is generally understood to be the total amount of greenhouse gas (GHG) emissions that are directly or indirectly caused by an individual, organization, product, or service. These emissions are typically measured in tonnes of carbon dioxide equivalent (CO2e).

- In 2009, the Greenhouse Gas Protocol (GHG Protocol) published a standard for calculating and reporting corporate carbon footprints. This standard is widely accepted by businesses and other organizations around the world. The GHG Protocol defines a carbon footprint as “the total set of greenhouse gas emissions caused by an organization, directly and indirectly, through its own operations and the value chain.”

- CO2e:

- CO2e means “carbon dioxide equivalent”. In layman’s terms, CO2e is a measurement of the total greenhouse gases emitted, expressed in terms of the equivalent measurement of carbon dioxide. On the other hand, CO2 only measures carbon emissions and does not account for any other greenhouse gases.

- A carbon dioxide equivalent or CO2 equivalent, abbreviated as CO2-eq is a metric measure used to compare the emissions from various greenhouse gases on the basis of their global-warming potential (GWP), by converting amounts of other gases to the equivalent amount of carbon dioxide with the same global warming potential.

- Carbon dioxide equivalents are commonly expressed as million metric tonnes of carbon dioxide equivalents, abbreviated as MMTCDE.

- The carbon dioxide equivalent for a gas is derived by multiplying the tonnes of the gas by the associated GWP: MMTCDE = (million metric tonnes of a gas) * (GWP of the gas).

- For example, the GWP for methane is 25 and for nitrous oxide 298. This means that emissions of 1 million metric tonnes of methane and nitrous oxide respectively is equivalent to emissions of 25 and 298 million metric tonnes of carbon dioxide.

- Carbon Credits or Carbon Offsets:

- Permits that allow the owner to emit a certain amount of carbon dioxide or other greenhouse gases. One credit permits the emission of one ton of carbon dioxide or the equivalent in other greenhouse gases.

- The carbon credit is half of a so-called cap-and-trade program. Companies that pollute are awarded credits that allow them to continue to pollute up to a certain limit, which is reduced periodically. Meanwhile, the company may sell any unneeded credits to another company that needs them. Private companies are thus doubly incentivized to reduce greenhouse emissions. First, they must spend money on extra credits if their emissions exceed the cap. Second, they can make money by reducing their emissions and selling their excess allowances.

- Kilowatt (kW):

- A kilowatt is simply a measure of how much power an electric appliance consumes—it’s 1,000 watts to be exact. You can quickly convert watts (W) to kilowatts (kW) by diving your wattage by 1,000: 1,000W 1,000 = 1 kW.

- Megawatt (MW):

- One megawatt equals one million watts or 1,000 kilowatts, roughly enough electricity for the instantaneous demand of 750 homes at once.

- Gigawatt (GW):

- A gigawatt (GW) is a unit of power, and it is equal to one billion watts.

- According to the Department of Energy, generating one GW of power takes over three million solar panels or 310 utility-scale wind turbines

- Terawatt (TW):

- One terawatt is equal to 1,000,000,000,000 watts.

- The main use of terawatts is found in the electric power industry.

- According to the United States Energy Information Administration, America is one of the largest electricity consumers in the world using about 4,146.2 terawatt-hours.

- Global Warming:

- Global warming is the long-term heating of Earth’s climate system observed since the pre-industrial period (between 1850 and 1900) due to human activities, primarily fossil fuel burning, which increases heat-trapping greenhouse gas levels in Earth’s atmosphere.

- Global Warming Potential (GWP):

- The heat absorbed by any greenhouse gas in the atmosphere, as a multiple of the heat that would be absorbed by the same mass of carbon dioxide (CO2). GWP is 1 for CO2. For other gases it depends on the gas and the time frame.

- Carbon dioxide equivalent (CO2e or CO2eq or CO2-e) is calculated from GWP. For any gas, it is the mass of CO2 which would warm the earth as much as the mass of that gas. Thus it provides a common scale for measuring the climate effects of different gases. It is calculated as GWP times mass of the other gas. For example, if a gas has GWP of 100, two tonnes of the gas have CO2e of 200 tonnes.

- GWP was developed to allow comparisons of the global warming impacts of different gases.

- Greenhouse Gas (GHG):

- A greenhouse gas is any gaseous compound in the atmosphere that is capable of absorbing infrared radiation, thereby trapping and holding heat in the atmosphere. By increasing the heat in the atmosphere, greenhouse gases are responsible for the greenhouse effect, which ultimately leads to global warming.

- The main gases responsible for the greenhouse effect include carbon dioxide, methane, nitrous oxide, and water vapor (which all occur naturally), and fluorinated gases (which are synthetic).

- GHG Protocol Corporate Standard Scope 1, 2 and 3: https://ghgprotocol.org/ + The GHG Protocol Corporate Accounting and Reporting Standard provides requirements and guidance for companies and other organizations preparing a corporate-level GHG emissions inventory. Scope 1 and 2 are mandatory to report, whereas scope 3 is voluntary and the hardest to monitor.

- Scope 1: Direct emissions:

- Direct emissions from company-owned and controlled resources. In other words, emissions are released into the atmosphere as a direct result of a set of activities, at a firm level. It is divided into four categories:

- Stationary combustion (e.g fuels, heating sources). All fuels that produce GHG emissions must be included in scope 1.

- Mobile combustion is all vehicles owned or controlled by a firm, burning fuel (e.g. cars, vans, trucks). The increasing use of “electric” vehicles (EVs), means that some of the organisation fleets could fall into Scope 2 emissions.

- Fugitive emissions are leaks from greenhouse gases (e.g. refrigeration, air conditioning units). It is important to note that refrigerant gases are a thousand times more dangerous than CO2 emissions. Companies are encouraged to report these emissions.

- Process emissions are released during industrial processes, and on-site manufacturing (e.g. production of CO2 during cement manufacturing, factory fumes, chemicals).

- Direct emissions from company-owned and controlled resources. In other words, emissions are released into the atmosphere as a direct result of a set of activities, at a firm level. It is divided into four categories:

- Scope 2: Indirect emissions – owned:

- Indirect emissions from the generation of purchased energy, from a utility provider. In other words, all GHG emissions released in the atmosphere, from the consumption of purchased electricity, steam, heat and cooling. For most organisations, electricity will be the unique source of scope 2 emissions. Simply stated, the energy consumed falls into two scopes: Scope 2 covers the electricity consumed by the end-user. Scope 3 covers the energy used by the utilities during transmission and distribution (T&D losses).

- Scope 3: Indirect emissions – not owned:

- Indirect emissions – not included in scope 2 – that occur in the value chain of the reporting company, including both upstream and downstream emissions. In other words, emissions are linked to the company’s operations. According to GHG protocol, scope 3 emissions are separated into 15 categories.

- Scope 1: Direct emissions:

- Environmental Health and Safety (EHS):

- General term used to refer to laws, rules, regulations, professions, programs, and workplace efforts to protect the health and safety of employees and the public as well as the environment from hazards associated with the workplace.

- The goal of an EHS management system is to protect workers from job-related injuries and illnesses, identify and mitigate physical, chemical and biological hazards in the workplace as well as improving training and communications that clearly explain the company objectives for promoting a safe and healthy work.

- There are 5 of the most common types of EHS (Environment, Health and Safety) Regulations: Occupational Safety and Health Regulations; Environmental Protection Regulations; Product Safety Regulations; Transportation Safety Regulations; Fire Safety Regulations.