Eaton – Eaton advances 2030 growth strategy with announcement to combine Mobility Group with Dana Incorporated

- Enhances Eaton’s focus on higher growth, higher margin Electrical and Aerospace businesses directly aligned to secular megatrends

- Immediately accretive to Eaton’s organic growth rate and operating margins upon closing, expected in the first quarter of 2027

- Reverse Morris Trust transaction values combined company at over $10 billion in enterprise value and Eaton’s Mobility Group at approximately $5.1 billion

- Eaton to receive an approximately $1.1 billion cash distribution; Eaton shareholders to own at least 50.1% of the combined company

- Combined company shareholders to benefit from $250 million of run-rate synergies

DUBLIN – Intelligent power management company Eaton (NYSE: ETN) today announced the next step in Eaton’s ongoing portfolio transformation. Eaton entered into a definitive agreement with Dana Incorporated (NYSE: DAN) under which Eaton will separate and combine its Mobility Group with Dana in a Reverse Morris Trust (RMT) transaction creating a combined company valued at over $10 billion.

The separation of the Mobility Group marks the next step in Eaton’s ongoing portfolio transformation and positions Eaton to execute on the Company’s 2030 growth strategy. Upon closing of the transaction, Eaton will operate a more focused portfolio concentrated on its Electrical and Aerospace businesses, which are directly aligned to secular growth themes in electrification, digitalization, AI-driven data center buildout, infrastructure modernization, aerospace aftermarket, and defense spending. The recent acquisitions of Ultra PCS and Boyd Thermal further strengthen the Company’s strategic positioning, extending Eaton’s capabilities in aerospace electronic controls and liquid cooling for data centers.

The separation is expected to be immediately accretive to Eaton’s organic growth rate and operating margins upon closing. Eaton expects to deploy the approximately $1.1 billion cash distribution from the transaction consistent with its existing capital allocation framework and priorities, including repayment of outstanding indebtedness.

Paulo Ruiz, Eaton chief executive officer, said, “We are pleased to have reached this agreement, which delivers significant value to Eaton and its shareholders, and represents a major milestone in Eaton’s 2030 growth strategy to lead, invest, and execute for growth. Eaton shareholders will benefit from the meaningful upside created by the combined company, and the transaction will provide substantial cash value for Eaton to deploy to our highest-growth and highest-margin opportunities. Looking ahead, our portfolio will be closely aligned with the powerful megatrends driving generational growth in our Electrical and Aerospace businesses, and we look forward to continuing our momentum to drive meaningful value for our customers and shareholders.”

Benefits of Combining Mobility Group and Dana

The combined Mobility Group and Dana will be a scaled, global engineered solutions partner, well-positioned to serve commercial vehicle and light vehicle OEMs worldwide. Together, the combined company will offer a comprehensive and complementary portfolio of drivetrain, propulsion, electrification, and power management solutions spanning internal combustion, hybrid, and fully electric platforms to commercial vehicle and automotive OEMs, supported by comprehensive technology capabilities and best in class manufacturing capabilities. The combined company expects to generate approximately $11 billion in pro forma revenue and $1.7 billion in pro forma estimated 2026 adjusted EBITDA (including run-rate synergies, which are expected to be fully realized within 24 months following closing).

The combined company will benefit from increased scale, $250 million of run-rate cost synergies, and greater diversification across customers, geographies, and end markets. It will also have an expanded aftermarket presence, which is expected to deliver more resilient revenue streams across economic cycles.

Mr. Ruiz continued, “Combining the Mobility Group with Dana creates a strong company that will be well-positioned to serve customers and support employees over the long term. We are proud of our mobility team and what they have built and are confident the combination of talent, capabilities, and technologies will create meaningful value for shareholders, customers, and employees alike.”

R. Bruce McDonald, Dana Chairman and Chief Executive Officer, stated, “We are excited to bring together Eaton’s Mobility Group with Dana. The addition of Mobility Group’s leading positions in commercial vehicle transmissions, clutches, and power management technologies, combined with Dana’s strengths in axles, driveshafts, electrification, thermal management, and sealing products, will create a truly differentiated global platform. Together, we will be better positioned to serve our customers, invest in innovation, and drive long-term value creation for shareholders of the combined company.”

Transaction Details

The transaction values Eaton’s Mobility Group at approximately $5.1 billion. This represents a multiple of 8.3x 2026 estimated pro forma adjusted EBITDA, or 5.9x on a fully synergized basis, including $250 million of run-rate synergies. Eaton shareholders will receive newly issued shares of the combined company such that Eaton shareholders will own at least 50.1% of the combined company’s outstanding shares following the consummation of the transaction. The agreement follows Eaton’s previously announced intent to separate its Mobility Group into an independent, publicly traded company.

The transaction is structured as a “Reverse Morris Trust” transaction, where Eaton will first separate its Mobility Group to Eaton shareholders through either an exchange offer (split-off) or a pro rata distribution (spin-off), at Eaton’s election. Immediately thereafter, Dana will merge with a subsidiary of the Mobility Group, with Dana surviving as a wholly owned subsidiary of the Mobility Group. In the event of a split-off, Eaton shareholders would have the opportunity to tender their Eaton shares in exchange for shares of the Mobility subsidiary. In the event of a spin-off, all Eaton shareholders would receive shares of the Mobility subsidiary on a pro rata basis. Eaton will also receive a cash distribution of $1.1 billion prior to completion of the transaction, subject to adjustment for cash and indebtedness, which will be funded by newly-issued debt of the Mobility Group. The transaction is intended to be tax-free for U.S. federal income tax purposes to Eaton and Eaton’s shareholders.

The agreement was unanimously approved by the Eaton board of directors following a comprehensive evaluation of strategic alternatives for its Mobility Group. The agreement was also unanimously approved by the Dana board of directors.

The transaction is expected to close in the first quarter of 2027, subject to receipt of Dana shareholder approval, receipt of required regulatory clearances, and customary closing conditions.

Byron Foster, Dana’s incoming Chief Executive Officer, and Timothy Kraus, Dana’s current Chief Financial Officer, will lead the combined company as CEO and CFO, respectively. Erin Rowse, Eaton’s current Senior Vice President Human Resources, Industrial, will serve as the combined company’s Chief Human Resources Officer upon close. The combined company’s senior management team will include representatives from both companies and will be announced as integration planning progresses. R. Bruce McDonald, Dana’s current Chairman and Chief Executive Officer, will serve as Executive Chairman of the combined company. Dana’s eight-member board of directors will be expanded to include three additional directors designated by Eaton, including one current Eaton executive and two current Eaton directors.

The combined company will operate as Dana Incorporated and will continue to be listed on the NYSE under the ticker symbol DAN.

In a separate press release and presentation issued today, Dana provided additional details regarding the combination.

Advisors

Morgan Stanley & Co. LLC is serving as Eaton’s financial advisor on the transaction and Paul, Weiss, Rifkind, Wharton & Garrison LLP and Hogan Lovells are acting as legal counsel to Eaton. Joele Frank, Wilkinson Brimmer Katcher is serving as Eaton’s strategic communications advisor.

Cautionary Notes on Forward-Looking Statements

This communication includes “forward-looking statements” within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended by the Private Securities Litigation Reform Act of 1995, including statements regarding the proposed transaction between Eaton Corporation plc (“Eaton”), Dana Incorporated (“Dana”) and Mobility (USA) Corporation (“SpinCo”). These forward-looking statements generally are identified by the words “believe,” “project,” “expect,” “anticipate,” “estimate,” “forecast,” “outlook,” “target,” “endeavor,” “seek,” “predict,” “intend,” “strategy,” “plan,” “may,” “could,” “should,” “will,” “would,” or the negative thereof or variations thereon or similar terminology generally intended to identify forward-looking statements. All statements, other than historical facts, including, but not limited to, statements regarding the expected timing and structure of the proposed transaction and financing of the transaction, the ability of the parties to complete the proposed transaction, the expected benefits of the proposed transaction, including future financial and operating results and strategic and synergistic benefits, the tax consequences of the proposed transaction, and the combined company’s plans, objectives, expectations and intentions, legal, economic and regulatory conditions, and any assumptions underlying any of the foregoing, are forward looking statements.

These forward-looking statements are based on Eaton’s and Dana’s current expectations and are subject to risks and uncertainties. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those indicated or anticipated by such forward-looking statements. The inclusion of such statements should not be regarded as a representation that such plans, estimates or expectations will be achieved. Important factors that could cause actual results to differ materially from such plans, estimates or expectations include, among others, the ability to complete the proposed transaction on the timeframe or on the terms currently anticipated or at all, including due to a failure to obtain requisite stockholder and/or regulatory approvals; risks related to difficulties, inabilities or delays in integrating the businesses of Dana and SpinCo; the ability to realize the anticipated benefits of the proposed transaction, including estimated combined EBITDA, estimated combined revenue and estimated run-rate cost synergies; potential impact of the announcement or consummation of the proposed transaction on Eaton’s and Dana’s stock prices; restrictions on the conduct of Eaton’s and Dana’s respective businesses prior to closing and on each of their ability to pursue alternatives to the proposed transaction; the possibility that the proposed transaction may be more expensive to complete than anticipated, including as a result of unexpected factors or events, or unforeseen or unknown liabilities; the ability of the combined company to implement its business strategy; the inability of the combined company to retain and hire key personnel; the occurrence of any event that could give rise to termination of the proposed transaction; the risk that stockholder litigation in connection with the proposed transaction or other litigation, settlements or investigations may affect the timing or occurrence of the proposed transaction or result in significant costs of defense, indemnification and liability; risks relating to the ability to obtain financing for the transaction upon acceptable terms or at all; evolving legal, regulatory and tax regimes; changes in general economic and/or industry specific conditions; global economic repercussions related to U.S. and global inflationary pressures and potential recessionary concerns; the risks that the anticipated tax treatment of the proposed transaction is not obtained; the risk of greater than expected difficulty in separating the business of SpinCo from the other businesses of Eaton; risks related to the disruption of management time from ongoing business operations due to the pendency of the proposed transaction, or other effects of the pendency of the proposed transaction on the relationship of any of the parties to the transaction with their employees, customers, suppliers, or other counterparties; and other risk factors detailed from time to time in Eaton’s and Dana’s reports filed with the Securities and Exchange Commission (the “SEC”), including Eaton’s and Dana’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and other documents filed with the SEC, including documents that will be filed with the SEC in connection with the proposed transaction. The foregoing list of important factors is not exclusive.

Any forward-looking statements speak only as of the date of this communication. None of Eaton, Dana or SpinCo undertakes, and each party expressly disclaims, any obligation to update any forward-looking statements, whether as a result of new information or development, future events or otherwise, except as required by law. Readers are cautioned not to place undue reliance on any of these forward-looking statements.

It should also be noted that projected financial information for the combined company is based on management’s estimates, assumptions and projections and has not been prepared in conformance with the applicable accounting requirements of Regulation S-X relating to pro forma financial information, and the required pro forma adjustments have not been applied and are not reflected therein. None of this information should be considered in isolation from, or as a substitute for, the historical financial statements of Dana or SpinCo.

Important Information About the Transaction and Where to Find It

In connection with the proposed transaction, SpinCo may file with the SEC an information statement on Form 10 (“Form 10”) or a registration statement on Form S-1/S-4 (the “Form S-1/S-4”) that constitutes a prospectus with respect to the shares of common stock, par value $0.01 per share, of SpinCo (the “SpinCo shares”) to be issued to Eaton shareholders in the proposed exchange offer (the “prospectus/offer to exchange”). Eaton may also file with the SEC a tender offer statement (the “Schedule TO”) with respect to the offer by Eaton to exchange all SpinCo shares for ordinary shares, par value $0.01 per share, of Eaton that are validly tendered and not properly withdrawn prior to the expiration of the exchange offer (if any). In addition, SpinCo intends to file with the SEC a registration statement on Form S-4 (the “Form S-4”) that will include a proxy statement of Dana and that also constitutes a prospectus of SpinCo with respect to the SpinCo shares to be issued in the proposed merger (the “proxy statement/prospectus”). Each of Eaton, SpinCo and Dana may also file other relevant documents with the SEC regarding the proposed transaction. This document is not a substitute for the Form 10, Form S-1/S-4, Schedule TO, Form S-4, prospectus/offer to exchange, proxy statement/prospectus or any other document that Eaton, SpinCo or Dana may file with the SEC. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENTS, THE SCHEDULE TO; THE PROSPECTUS/OFFER TO EXCHANGE, THE PROXY STATEMENT/PROSPECTUS AND ANY OTHER RELEVANT DOCUMENTS THAT MAY BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY IF AND WHEN THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT EATON, DANA, SPINCO AND THE PROPOSED TRANSACTION. Investors and security holders will be able to obtain free copies of the Form 10, Form S-1/S-4, Schedule TO, Form S-4, the prospectus/offer to exchange and the proxy statement/prospectus (if and when available) and other documents containing important information about Eaton, Dana and SpinCo and the proposed transaction, once such documents are filed with the SEC through the website maintained by the SEC at http://www.sec.gov. Copies of the documents filed with, or furnished to, the SEC by Eaton and SpinCo will be available free of charge on Eaton’s website at https://www.eaton.com/us/en-us/company/investor-relations.html. Copies of the documents filed with, or furnished to, the SEC by Dana will be available free of charge on Dana’s website at https://danaincorporated.gcs-web.com/. The information included on, or accessible through, Eaton or Dana’s website is not incorporated by reference into this communication.

Participants in the Solicitation

Eaton, Dana, SpinCo and certain of their respective directors and executive officers may be deemed to be participants in the solicitation of proxies in respect of the proposed transaction. Information about the directors and executive officers of Eaton, including a description of their direct or indirect interests, by security holdings or otherwise, is set forth in Eaton’s proxy statement for its 2026 Annual General Meeting of Shareholders, which was filed with the SEC on March 13, 2026. Information about the directors and executive officers of Dana, including a description of their direct or indirect interests, by security holdings or otherwise, is set forth in Dana’s proxy statement for its 2026 Annual Meeting of Stockholders, which was filed with the SEC on March 13, 2026. Other information regarding the participants in the proxy solicitation and a description of their direct and indirect interests, by security holdings or otherwise, will be contained in the Form S-4 and the proxy statement/prospectus and other relevant materials to be filed with the SEC regarding the proposed transaction when such materials become available. Investors should read the Form 10, Form S-1/S-4, Schedule TO, Form S-4, the prospectus/offer to exchange and the proxy statement/prospectus carefully if and when available before making any voting or investment decisions. You may obtain free copies of these documents from Eaton or Dana using the sources indicated above.

No Offer or Solicitation

This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy or exchange any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation, sale or exchange would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act or in a transaction exempt from the registration requirements of the Securities Act.

Note Regarding Use of Non-GAAP Financial Measures

In addition to the financial measures presented in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”), this communication includes certain non-GAAP financial measures (collectively, the “Non-GAAP Measures”), such as adjusted EBITDA. These Non-GAAP Measures should not be used in isolation or as a substitute or alternative to results determined in accordance with U.S. GAAP. In addition, Dana’s and Eaton’s definitions of these Non-GAAP Measures may not be comparable to similarly titled non-GAAP financial measures reported by other companies. A reconciliation of these Non-GAAP Measures to the most directly comparable financial measures calculated and reported in accordance with U.S. GAAP can be found in Dana’s filings with the SEC except for financial guidance and other forward-looking information since such a reconciliation is not practicable without unreasonable effort as Dana is unable to reasonably forecast certain amounts that are necessary for such reconciliation.

SourceEaton

EMR Analysis

More information on Eaton: See full profile on EMR Executive Services

More information on Gregory R. Page (Non-Executive Chairman of the Board, Eaton): See the full profile on EMR Executive Services

More information on Paulo Ruiz Sternadt (Chief Executive Officer, Eaton): See the full profile on EMR Executive Services

More information on David Foster (Senior Leadership Team – Executive Vice President and Chief Financial Officer, Eaton): See full profile on EMR Executive Services

More information on Eaton’s 2030 Growth Strategy (Lead, Invest and Execute for Growth) by Eaton: See full profile on EMR Executive Services

More information on Eaton Mobility Group by Eaton: https://www.eaton.com/us/en-us/company/careers/experienced-professionals/mobility.html + No specific website available yet + Eaton’s Mobility Group (previously named separately Eaton Vehicle Business and Eaton E-Mobility Business) includes our Vehicle and eMobility businesses, representing the company’s focus on providing solutions across the propulsion spectrum and meeting the evolving needs of its customers, from internal combustion to electrified or a combination of both.

To support increasing degrees of electrification, the Mobility Group offers a suite of technologies, including power distribution solutions, power electronics and transmissions that improve safety, efficiency, and performance.

Power connection solutions were introduced following the acquisition in 2022 of Royal Power Solutions, a global leader in the development and production of critical high-precision power- and signal-distribution components.

The principal markets for the Mobility Group are original equipment manufacturers of on- and off-highway vehicles and aftermarket customers.

- Our Vehicle business designs, develops, and manufactures technologies for the global automotive, commercial vehicle, aftermarket, and off-highway markets. Eaton delivers differentiated solutions to improve fuel economy and efficiency through technologies including transmissions, clutches, engine air management, fuel emissions and torque control products.

- Our eMobility business delivers innovative technologies to the automotive and commercial vehicle markets by combining the expertise and global manufacturing capabilities from Eaton’s Electrical and Vehicle businesses. Eaton provides a portfolio of high voltage power distribution & protection, power connection, power electronics, 48V, and low voltage solutions for original equipment manufacturers.

After the spin-off, Eaton’s Mobility Group will be a global engineered solutions partner to commercial vehicle, automotive and off-highway OEMs, with strong market position and industry leading technologies

More information on Antonio Galvao (Senior Leadership Team – President, Mobility Group, Eaton): See the full profile on EMR Executive Services

More information on Benjamin Karrer (Director, Power Distribution and Protection, Mobility Group, Eaton): See the full profile on EMR Executive Services

More information on Eaton eMobility Business by Eaton Mobility Group by Eaton: https://www.eaton.com/us/en-us/products/emobility/expertise.html?wtredirect=www.eaton.com/eMobility + Eaton’s eMobility business was formed by combining products, expertise and global manufacturing capabilities from Eaton’s Electrical and Vehicle Groups. Eaton plans to further develop new products and technologies, including smart diagnostics, intelligent power electronics and predictive health monitoring systems, to strengthen its global capabilities and deliver intelligent electrification solutions to passenger car, commercial vehicle and off-highway customers.

The principal markets for the Mobility Group are original equipment manufacturers of on- and off-highway vehicles and aftermarket customers.

More information on Mark Schneider (President, eMobility Business, Eaton Mobility Group, Eaton): See full profile on EMR Executive Services

More information on Electrical Sector by Eaton: See the full profile on EMR Executive Services

More information on Heath Monesmith (Senior Leadership Team – President and Chief Operating Officer, Electrical Sector + Corporate Responsibility for Eaton’s Europe, Middle East and Africa Region, Eaton): See the full profile on EMR Executive Services

More information on Aerospace Group by Eaton: See the full profile on EMR Executive Services

More information on John Sapp (Senior Leadership Team – President, Aerospace Group, Eaton): See the full profile on EMR Executive Services

More information on Ultra PCS Limited by Eaton: See the full profile on EMR Executive Services

More information on Boyd Thermal Business by Eaton: See the full profile on EMR Executive Services

More information on Erin Rowse (Senior Vice President Human Resources, Industrial Sector, Eaton): See the full profile on EMR Executive Services

More information on Dana Incorporated: https://www.dana.com/ + Dana Incorporated (NYSE: DAN) is a global leader in the design and manufacture of highly efficient propulsion solutions for the light- and commercial‑vehicle markets. Guided by its vision to be the world’s best powertrain company, Dana delivers advanced conventional and clean‑energy technologies that help customers improve the performance, efficiency, and durability of their vehicles. The company supplies leading vehicle manufacturers and related aftermarkets with industry‑defining drive systems, electrodynamic technologies, and thermal and sealing solutions.

Headquartered in Maumee, Ohio, USA, Dana reported sales of $7.5 billion in 2025. With a history dating to 1904, the company employs 27,000 people in 24 countries across six continents.

More information on R. Bruce McDonald (Chairman and Chief Executive Officer, Dana Incorporated till July 1, 2026 + Chairman, Dana Incorporated as from July 1, 2026): https://www.dana.com/newsroom/press-releases/dana-incorporated-announces-appointment-of-byron-foster-as-chief-executive-officer/ + https://www.dana.com/company/leadership/

More information on Byron Foster (Senior Vice President and President, Light Vehicle Systems, Dana Incorporated till July 1, 2026 + Chief Executive Officer, Dana Incorporated as from July 1, 2026): https://www.dana.com/newsroom/press-releases/dana-incorporated-announces-appointment-of-byron-foster-as-chief-executive-officer/ + https://www.dana.com/company/leadership/ + https://www.linkedin.com/in/byron-foster-6042ab15/

More information on Timothy Kraus (Chief Financial Officer, Dana Incorporated): https://www.dana.com/company/leadership/ + https://www.linkedin.com/in/timothy-kraus-a0b42522/

EMR Additional Notes:

- Morris Trust and Reverse Morris Trust (RMT):

- A Morris Trust and a Reverse Morris Trust (RMT) are both tax-free corporate restructuring strategies used to divest assets, but they differ entirely in which entity combines with a third party.

- In a standard Morris Trust, the parent company merges with a buyer after spinning off unwanted assets.

- In a Reverse Morris Trust, the spun-off subsidiary merges with a buyer while the parent remains independent.

- A Morris Trust and a Reverse Morris Trust (RMT) are both tax-free corporate restructuring strategies used to divest assets, but they differ entirely in which entity combines with a third party.

- AI – Artificial Intelligence:

- Artificial Intelligence (AI) is the broad field of computer science focused on building systems that perform tasks requiring human-like intelligence, such as learning, reasoning, perception, and decision-making.

- AI systems typically:

- ingest large datasets

- identify patterns

- make predictions or decisions

- AI is an umbrella term that includes machine learning, deep learning, and other approaches (rule-based systems, optimization, etc.), not just Machine Learning (ML).

- AI programming focuses on three cognitive skills: learning, reasoning and self-correction.

- The 4 types of artificial intelligence?

- Type 1: Reactive machines. These AI systems have no memory and are task specific. An example is Deep Blue, the IBM chess program that beat Garry Kasparov in the 1990s. Deep Blue can identify pieces on the chessboard and make predictions, but because it has no memory, it cannot use past experiences to inform future ones.

- Type 2: Limited memory. Most modern AI systems. These AI systems have memory, so they can use past experiences to inform future decisions. Some of the decision-making functions in self-driving cars are designed this way.

- Type 3: Theory of mind. Research stage. Theory of mind is a psychology term. When applied to AI, it means that the system would have the social intelligence to understand emotions. This type of AI will be able to infer human intentions and predict behavior, a necessary skill for AI systems to become integral members of human teams.

- Type 4: Self-awareness. Does not yet exist. In this category, AI systems have a sense of self, which gives them consciousness. Machines with self-awareness understand their own current state.

- Machine Learning (ML):

- Subset of AI that enables systems to learn from data without explicit programming.

- ML uses historical data to detect patterns and make predictions.

- ML is the dominant paradigm in modern AI, replacing most rule-based systems.

- ML allows software applications to become more accurate at predicting outcomes without being explicitly programmed to do so.

- Recommendation engines are a common use case for ML. Other uses include fraud detection, spam filtering, business process automation (BPA) and predictive maintenance.

- Classical ML is often categorized by how an algorithm learns to become more accurate in its predictions. There are four basic approaches:

- supervised learning,

- unsupervised learning,

- semi-supervised learning and

- reinforcement learning.

- Deep Learning (DL):

- Subset of ML using multi-layered neural networks to learn complex representations.

- DL is not always “more sophisticated” in all contexts—it is more powerful for unstructured data (images, text, audio), but classical ML can outperform it in structured/tabular data.

- DL makes use of layers of information processing, each gradually learning more and more complex representations of data. The early layers may learn about colors, the next ones about shapes, the following about combinations of those shapes, and finally actual objects. DL demonstrated a breakthrough in object recognition. Face recognition is a good example.

- DL is currently the most sophisticated AI architecture we have developed.

- Generative AI (GenAI):

- AI systems that generate new content (text, images, code, audio, etc.) based on learned patterns.

- GenAI is typically powered by large deep learning models (e.g., transformers), not a separate paradigm.

- Generative AI technology generates outputs based on some kind of input – often a prompt supplied by a person. Some GenAI tools work in one medium, such as turning text inputs into text outputs, for example. With the public release of ChatGPT in late November 2022, the world at large was introduced to an AI app capable of creating text that sounded more authentic and less artificial than any previous generation of computer-crafted text.

- Small Language Models (SLM) and Large Language Models (LLM):

- Small Language Models (SLMs) are artificial intelligence (AI) models capable of processing, understanding and generating natural language content. As their name implies, SLMs are smaller in scale and scope than large language models (LLMs).

- LLM means Large Language Models — a type of machine learning/deep learning model that can perform a variety of natural language processing (NLP) and analysis tasks, including translating, classifying, and generating text; answering questions in a conversational manner; and identifying data patterns.

- For example, virtual assistants like Siri, Alexa, or Google Assistant use LLMs to process natural language queries and provide useful information or execute tasks such as setting reminders or controlling smart home devices.

- Computer Vision (CV) / Vision AI & Machine Vision (MV):

- Broad AI field for interpreting visual data.

- Field of AI that enables computers to interpret and act on visual data (images, videos). It works by using deep learning models trained on large datasets to recognize patterns, objects, and context.

- The most well-known case of this today is Google’s Translate, which can take an image of anything — from menus to signboards — and convert it into text that the program then translates into the user’s native language.

- Machine Vision (MV) :

- lndustrial application of Computer Vision. MV is a subset of CV, not a parallel category.

- Specific application for industrial settings, relying on cameras to analyze tasks in manufacturing, quality control, and worker safety. The key difference is that CV is a broader field for extracting information from various visual inputs, while MV is more focused on specific industrial tasks.

- Machine Vision is the ability of a computer to see; it employs one or more video cameras, analog-to-digital conversion and digital signal processing. The resulting data goes to a computer or robot controller. Machine Vision is similar in complexity to Voice Recognition.

- Multimodal Intelligence and Agents:

- Subset of artificial intelligence that integrates multiple data types (text, image, audio, video).

- Multimodal capabilities allows AI to interact with users in a more natural and intuitive way. It can see, hear and speak, which means that users can provide input and receive responses in a variety of ways.

- An AI agent is a computational entity designed to act independently. It performs specific tasks autonomously by making decisions based on its environment, inputs, and a predefined goal. What separates an AI agent from an AI model is the ability to act. There are many different kinds of agents such as reactive agents and proactive agents. Agents can also act in fixed and dynamic environments. Additionally, more sophisticated applications of agents involve utilizing agents to handle data in various formats, known as multimodal agents and deploying multiple agents to tackle complex problems.

- The defining feature of an agent is not just decision-making, but the ability to take actions toward a goal in an environment.

- Agentic AI:

- Agentic AI is a system that can accomplish a specific goal with limited supervision. It consists of AI agents—machine learning models that mimic human decision-making to solve problems in real time. In a multi-agent system, each agent performs a specific subtask required to reach the goal and their efforts are coordinated through AI orchestration.

- Unlike traditional AI models, which operate within predefined constraints and require human intervention, agentic AI exhibits autonomy, goal-driven behavior and adaptability. The term “agentic” refers to these models’ agency, or, their capacity to act independently and purposefully.

- Agentic AI builds on generative AI (gen AI) techniques by using large language models (LLMs) to function in dynamic environments. While generative models focus on creating content based on learned patterns, agentic AI extends this capability by applying generative outputs toward specific goals.

- Edge AI Technology:

- AI executed locally on devices (IoT, sensors, cameras) instead of centralized cloud.

- Edge AI refers to the deployment of AI algorithms and AI models directly on local edge devices such as sensors or Internet of Things (IoT) devices, which enables real-time data processing and analysis without constant reliance on cloud infrastructure.

- Simply stated, edge AI, or “AI on the edge“, refers to the combination of edge computing and artificial intelligence to execute machine learning tasks directly on interconnected edge devices. Edge computing allows for data to be stored close to the device location, and AI algorithms enable the data to be processed right on the network edge, with or without an internet connection. This facilitates the processing of data within milliseconds, providing real-time feedback.

- Self-driving cars, wearable devices, security cameras, and smart home appliances are among the technologies that leverage edge AI capabilities to promptly deliver users with real-time information when it is most essential.

- High-Density AI:

- High-density AI refers to the concentration of AI computing power and storage within a compact physical space, often found in specialized data centers. It is an infrastructure trend (AI data centers / GPU clusters), not a distinct AI category. This approach allows for increased computational capacity, faster training times, and the ability to handle complex simulations that would be impossible with traditional infrastructure.

- Explainable AI (XAI) and Human-Centered Explainable AI (HCXAI):

- Explainable AI (XAI) refers to methods for making AI model decisions understandable to humans, focusing on how the AI works, whereas Human-Centered Explainable AI (HCXAI) goes further by contextualizing those explanations to a user’s specific task and understanding needs.

- While XAI aims for technical transparency of the model, HCXAI emphasizes the human context, emphasizing user relevance, and the broader implications of explanations, including fairness, trust, and ethical considerations.

- Physical AI & Embodied AI:

- Physical AI refers to a branch of AI that enables machines to perceive, understand, and interact with the physical world by directly processing data from a variety of sensors and actuators.

- Embodied AI, as a subset, focuses on the sensory, decision-making, and interaction capabilities that enable these systems to function effectively in dynamic and unpredictable environments via sensors and actuators.

- Federated Learning and Reinforcement Learning:

- Federated Learning is a machine-learning technique where data stays where it is, and only the learned model updates are shared. “Training AI without sharing your data”.

- Reinforcement Learning is a type of AI where an agent learns by interacting with an environment and receiving rewards or penalties. “Learning by trial and error”

- Federated Learning (FL) and Reinforcement Learning (RL) can be combined into a field called Federated Reinforcement Learning (FRL), where multiple agents learn collaboratively without sharing their raw data. In this approach, each agent trains its own RL policy locally and shares model updates, like parameters or gradients, with a central server. The server aggregates these updates to create a more robust, global model. FRL is used in applications like optimizing resource management in communication networks and enhancing the performance of autonomous systems by learning from diverse, distributed experiences while protecting privacy (still niche and mostly experimental.)

- AI Factories:

- AI Factories are specialized, high-performance computing centers designed to train, tune, and deploy artificial intelligence models at scale.

- Companies and organizations involved in AI factory infrastructure and development include Nvidia, AWS, Microsoft, OpenAI, CoreWeave, Lambda, Nebius, Supermicro, and HPE. The European Union is also establishing AI Factories through its EuroHPC Joint Undertaking to foster regional innovation.

- “AI factory” is a conceptual term (not standardized), referring to industrial-scale AI production systems.

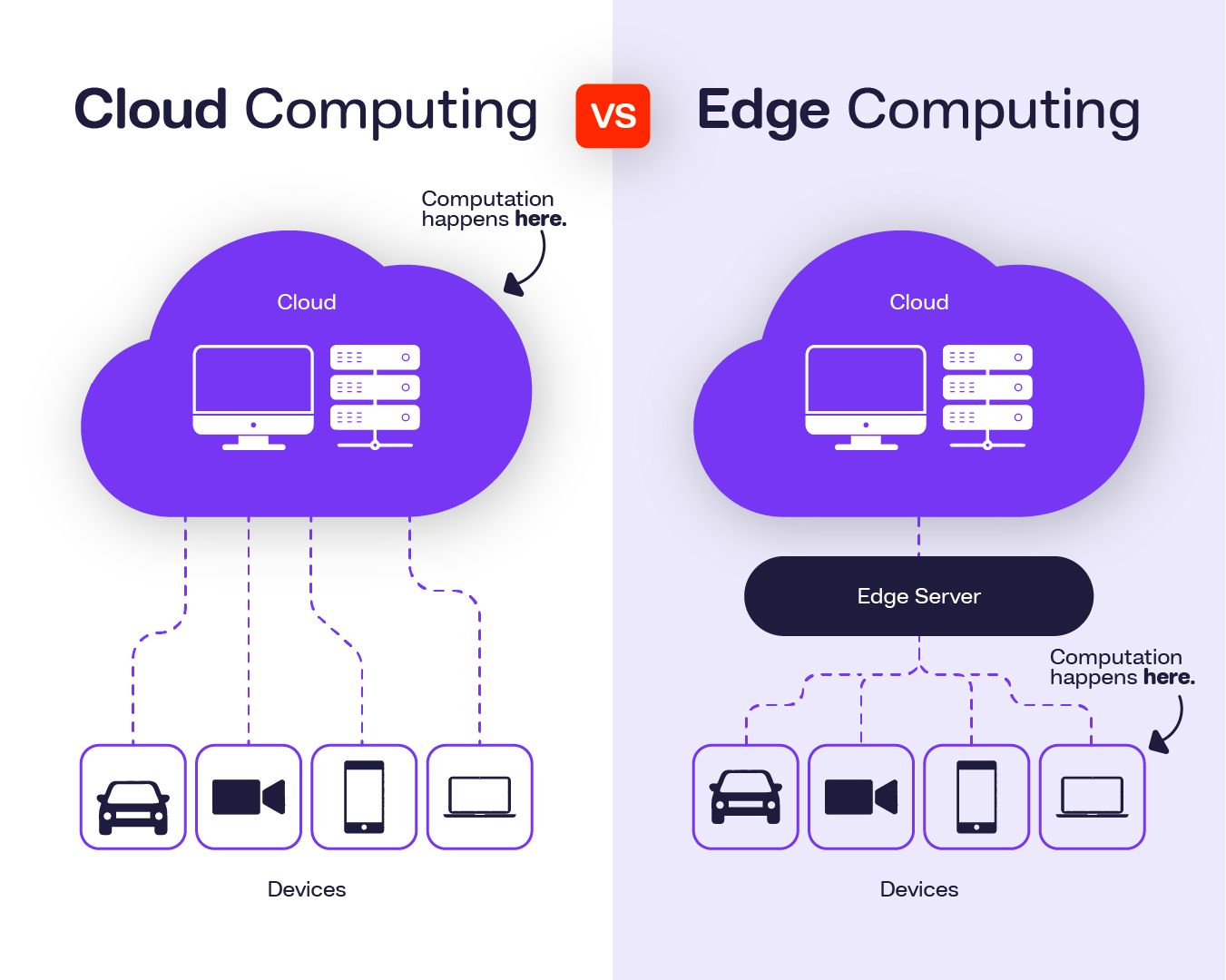

- Cloud Computing:

- Cloud computing is a general term for anything that involves delivering hosted services over the internet. It is the on-demand availability of computer system resources, especially data storage and computing power, without direct active management by the user. Large clouds often have functions distributed over multiple locations, each location being a data center. Cloud services typically include IaaS, PaaS, and SaaS service models.

- Edge Computing:

- Edge computing is a form of computing that is done on site or near a particular data source, minimizing the need for data to be processed in a remote data center.

- Edge computing can enable more effective city traffic management. Examples of this include optimising bus frequency given fluctuations in demand, managing the opening and closing of extra lanes, and, in future, managing autonomous car flows.

- An edge device is any piece of hardware that controls data flow at the boundary between two networks. Edge devices fulfill a variety of roles, depending on what type of device they are, but they essentially serve as network entry — or exit — points.

- There are five main types of edge computing devices: IoT sensors, smart cameras, uCPE equipment, servers and processors. IoT sensors, smart cameras and uCPE equipment will reside on the customer premises, whereas servers and processors will reside in an edge computing data centre.

- In service-based industries such as the finance and e-commerce sector, edge computing devices also have roles to play. In this case, a smart phone, laptop, or tablet becomes the edge computing device.

- Edge Devices:

- Edge devices encompass a broad range of device types, including sensors, actuators and other endpoints, as well as IoT gateways. Within a local area network (LAN), switches in the access layer — that is, those connecting end-user devices to the aggregation layer — are sometimes called edge switches.

- Edge devices act as the interface between the physical world (data generation) and digital networks.

- Hybrid Computing:

- A hybrid cloud integrates private, on-premises infrastructure with public cloud services, offering flexibility to distribute workloads between these environments. Hybrid models often incorporate edge computing, allowing organizations to run critical workloads locally at the edge while using the cloud for other tasks, thereby optimizing performance, cost, and data management for various business needs.

- HPC (Hight-Performance Computing):

- Practice of aggregating computing resources to gain performance greater than that of a single workstation, server, or computer. HPC can take the form of custom-built supercomputers or groups of individual computers called clusters.

- HPC is typically used for simulation, scientific computing, AI training, and complex modeling.

- Data Centers – Physical Infrastructure:

- A data center is a facility that centralizes an organization’s shared IT operations and equipment for the purposes of storing, processing, and disseminating data and applications. Because they house an organization’s most critical and proprietary assets, data centers are vital to the continuity of daily operations.

- Hyperscale Data Centers – Physical Infrastructure:

- The clue is in the name: hyperscale data centers are massive facilities built by companies with vast data processing and storage needs. These firms may derive their income directly from the applications or websites the equipment supports, or sell technology management services to third parties.

- Hyperscale Data Centers are typically operated by large cloud providers (e.g., hyperscalers) and designed for horizontal scalability.

- White Space and Grey Space in Data Centers – Physical Infrastructure:

- White space in a data center refers to the area where IT equipment is placed. It typically houses servers, storage, network gear, and racks.

- Gray space, on the other hand, is the area where the back-end infrastructure is located. This space is essential for supporting the IT equipment and includes areas for switchgear, UPS, transformers, chillers, and generators.

- Colocation in Data Centers – Physical Infrastructure:

- A colocation data center is a facility where businesses rent space, power, and cooling to house their own servers and networking hardware, rather than maintaining them in-house. It offers a cost-effective way to access high-level security, internet connectivity, and 24/7 technical support while retaining control of the equipment.

- Edge & Cloud Services – Integrated Architecture (Edge-to-Cloud):

- Edge services perform data processing on local devices and servers near the data source, reducing latency for time-sensitive operations, while cloud services centralize large computations and storage in remote datacenters, offering massive scalability and flexibility for general workloads.

- Most organizations use both, creating an “edge-to-cloud” architecture where edge devices handle immediate tasks, and the cloud manages large-scale data processing and complex applications, providing a seamless and efficient experience.

- Data Center Cooling Technologies:

- Air Cooling:

- Uses Computer Room Air Conditioners (CRAC) or Air Handlers (CRAH) combined with hot aisle / cold aisle containment to circulate cold air through the facility.

- It is widely used and cost-effective, but becomes inefficient at very high rack power densities (typically >20–30 kW per rack).

- Liquid Cooling:

- Liquid cooling uses water or dielectric fluids to remove heat more efficiently than air, enabling higher power densities required for AI and HPC workloads.

- Direct-to-Chip (DTC) Cooling:

- A Direct-to-Chip (DTC) cooling system is a liquid-cooling technology used to cool high-performance computer chips—such as CPUs, GPUs, and accelerators—by bringing a liquid coolant directly to the chip surface through a cold plate (heat exchanger attached to the chip).

- It is one of the most efficient and fastest-growing cooling methods in modern data centers, especially in AI, HPC (High-Performance Computing), and high-density server environments.

- RDHX (Rear Door Heat Exchanger) – Rack-level Heat Exchange:

- A Rear Door Heat Exchanger (RDHx) is a rack-mounted liquid-to-air heat exchanger installed on the rear of an IT rack.

- Chilled water flows through the door, and hot air from servers passes through it, removing heat before it enters the data center room (air-neutral or near-zero heat rejection to white space).

- Can be passive (no fans) or active (with fans)

- Enables high-density racks without requiring full liquid cooling at the chip level.

- HDU (Heat Dissipation Unit):

- Unlike a CDU that transfers heat to the facility water loop, a Heat Dissipation Unit (HDU) rejects heat from the server rack to the data center air (white space).

- This means heat is ultimately removed by room-level cooling systems (CRAC/CRAH), making it a hybrid approach between air and liquid cooling.

- CDU (Coolant Distribution Unit):

- A coolant distribution unit contains pumps, heat exchangers, valves, and control systems that circulate coolant through a network of pipes, distributing it to servers or racks.

- Coolant Distribution Units are essential in liquid-cooled data centers, providing:

- flow control

- pressure regulation

- temperature management

- hydraulic separation between facility loop and IT loop.

- They interface between facility water (building loop) and IT cooling loops, ensuring safe and controlled heat transfer.

- Chillers:

- Mechanical systems that remove heat from a building’s liquid coolant (typically water) and transfer it to the outside environment (via air or water loops).

- Unlike systems that cool air directly, chillers generate chilled water that circulates through cooling systems such as CDUs, CRAH/CRAC units, or heat exchangers.

- They are essential for cooling large-scale data centers and industrial facilities, especially where free cooling is not sufficient.

- Condensors:

- A condenser is a heat exchanger that cools a gas or vapor, causing it to condense into a liquid, releasing latent heat.

- In cooling systems, condensers are typically part of chiller or refrigeration cycles, where they reject heat to ambient air or water (e.g., cooling towers or dry coolers).

- Technology Cooling System (TCS):

- Non-standard / umbrella term that refers to an integrated cooling architecture used to manage heat in technology environments (e.g., data centers, industrial systems).

- A TCS may include:

- Chillers

- CDUs

- Pumps and piping

- Heat exchangers

- Control systems

- Air Cooling:

- OEM vs. MRO vs. Integrated Supply:

- OEM (Original Equipment Manufacturer):

- An Original Equipment Manufacturer (OEM) is a company that designs and/or manufactures products or components that are used in another company’s end product, which may be marketed under that company’s brand name. An OEM can produce complete systems or individual components.

- The term OEM usually refers to original, specification-compliant parts used in the initial production of equipment, whereas aftermarket refers to third-party products used as replacements or upgrades after the original sale.

- OEM (Original Equipment Manufacturer):

- MRO (Maintenance, Repair and Operations):

- MRO refers to all the activities and supplies needed to keep a company’s operations, facilities, and equipment running efficiently and safely.

- These are supplies used to support production but that do not become part of the final product.

- Examples of MRO items include:

- Maintenance tools

- Replacement/spare parts

- Personal protective equipment (PPE)

- Cleaning and facility supplies

- Office and operational consumables

- Integrated Supply:

- Integrated Supply is a service-based, end-to-end supply chain solution for managing MRO procurement and inventory in a more efficient and digitally connected way.

- The goal is to:

- reduce total cost of ownership (TCO)

- improve response time and availability

- optimize inventory levels (often vendor-managed inventory, VMI)

- increase operational efficiency

- It typically involves:

- on-site or embedded supplier presence

- digital integration between supplier and customer systems (ERP, inventory)

- real-time data sharing (inventory levels, consumption, orders)

- For example, a supplier’s system may be integrated with a buyer’s system to provide real-time visibility and automated replenishment of MRO items.

- => OEM vs. MRO vs. Integrated Supply:

- OEM: Builds/designs the product (or core components)

- MRO: Keeps operations running (non-production supplies)

- Integrated Supply: Optimizes how MRO is sourced, managed, and delivered

- Drivetrain or Transmission System:

- The drivetrain includes the transmission, driveshaft (for RWD/AWD vehicles), differential(s), axles, and wheels. It works in conjunction with the engine (or electric motor) to transmit power to the wheels. The drivetrain system is an essential component of a vehicle, and the transmission is one of its key subsystems (not the whole system).

- Essentially, the parts of a drivetrain work together to make a vehicle move by transmitting and modulating mechanical power from the engine to the wheels.

- It works as follows:

- The engine generates rotational power

- The transmission adjusts torque and speed (gear ratios) depending on driving conditions

- The driveshaft transmits this power (in certain vehicle layouts, e.g., RWD/AWD)

- The differential distributes power to the wheels while allowing them to rotate at different speeds

- The axles transfer torque to the wheels, causing them to rotate

- The vehicle moves forward based on the torque delivered to the wheels and the gear ratio selected, not simply the speed of the driveshaft.

- All these components work together to convert engine power into controlled vehicle motion, while the steering and braking systems independently control direction and speed.

- EBIT:

- Earnings Before Interest and Taxes (EBIT) is a measure of a company’s operating profitability before accounting for interest expenses and income taxes. It is also known as operating profit and shows how effectively a company’s core business is generating profit from its operations.

- EBITA:

- Earnings before interest, taxes, and amortization (EBITA) is a measure of company profitability used by investors. It is helpful for comparing one company to another in the same line of business.

- EBITA = Net income + Interest + Taxes + Amortization

- EBITDA:

- Earnings before interest, taxes, depreciation, and amortization (EBITDA) is an alternate measure of profitability to net income. By including depreciation and amortization as well as taxes and debt payment costs, EBITDA attempts to represent the cash profit generated by the company’s operations.

- EBITDA and EBITA are both measures of profitability. The difference is that EBITDA also excludes depreciation.

- EBITDA is the more commonly used measure because it adds depreciation—the accounting practice of recording the reduced value of a company’s tangible assets over time—to the list of factors.

- EV/EBITDA (Enterprise Multiple):

- Enterprise multiple, also known as the EV-to-EBITDA multiple, is a ratio used to determine the value of a company.

- It is computed by dividing enterprise value by EBITDA.

- The enterprise multiple takes into account a company’s debt and cash levels in addition to its stock price and relates that value to the firm’s cash profitability.

- Enterprise multiples can vary depending on the industry.

- Higher enterprise multiples are expected in high-growth industries and lower multiples in industries with slow growth.

- Spin-Off and Split-Off:

- A spin-off and a split-off are both corporate restructuring strategies used to separate a parent company from a subsidiary.

- The key difference lies in share distribution:

- A spin-off creates a new, independent company where existing shareholders automatically receive shares in the new entity on a pro-rata basis while retaining their shares in the parent company.

- A split-off is a transaction in which shareholders are offered (not forced) the option to exchange some or all of their parent company shares for shares in the new entity, meaning they end up holding either the parent company or the new company (or a mix, depending on participation).

- Generally Accepted Accounting Principles (GAAP):

- GAAP is the set of accounting rules and standards established by the Financial Accounting Standards Board (FASB) that U.S. companies are required (for public companies) or expected (for others) to follow when preparing financial statements.

- The goal of GAAP is to ensure that financial statements are:

- complete

- consistent

- comparable

- reliable and transparent

- GAAP may be contrasted with non-GAAP (pro forma) reporting, which adjusts standard results to exclude certain items for analytical purposes.

- GAAP is used primarily in the U.S., while most other countries follow International Financial Reporting Standards (IFRS).

- GAAP is also used by state and local governments, although these typically follow standards issued by the Governmental Accounting Standards Board (GASB).

- International Financial Reporting Standards (IFRS):

- IFRS is a globally recognized set of accounting standards used in most jurisdictions worldwide, including the European Union.

- It is issued by the International Accounting Standards Board (IASB) and is designed to make financial statements:

- consistent

- transparent

- comparable across countries

- IFRS replaced the earlier International Accounting Standards (IAS) framework in 2001.

- IFRS fosters greater corporate transparency by emphasizing principles-based accounting, allowing companies to apply judgment based on economic substance.

- Chinese companies primarily follow Chinese Accounting Standards (ASBE), which are largely converged with IFRS but not identical.

- => GAAP vs. IFRS:

- GAAP: U.S.-focused, more rules-based, highly detailed

- IFRS: Global, more principles-based, flexible application